☕ Daily Finance — 27 Feb 2026

AI stocks stumble. Bonds stir. Bitcoin cools. Markets recalibrate.

AI stocks blinked. Bonds stirred. Bitcoin cooled.

The market just shifted from “buy everything AI” to “prove it.”

Here’s what actually mattered today:

🚀 Nvidia crushes earnings… and still drops 5%

Nvidia delivered another monster quarter: revenue up ~73% YoY, data-center sales up ~75%, EPS beat expectations, and next-quarter guidance came in above forecasts.

Translation? AI infrastructure demand is still on fire.

So why did the stock fall ~5.5% to $184.89?

Because expectations were even hotter.

The selloff dragged the Nasdaq down 1.18% and pressured the broader AI complex.

Why it matters: The AI trade isn’t dead. It’s just expensive now. Markets want sustainability — not just surprise beats.

🔄 Rotation under the hood

Headline indexes looked weak, but underneath, something interesting happened.

While the S&P 500 slipped 0.54% and the Nasdaq fell, the Dow managed a slight gain. Financials, energy, and real estate quietly outperformed as investors rotated out of mega-cap AI names.

Even more telling? A majority of S&P components actually finished higher.

Why it matters: This looks more like profit-taking and broadening leadership — not the end of the bull run.

🖥 AI divergence: CoreWeave tumbles, Dell surges

CoreWeave reported +110% YoY revenue growth and a massive $67B backlog. Impressive.

But shares dropped ~8% after 2026 guidance only slightly topped expectations — and investors focused on its $21.4B debt load.

Meanwhile, Dell posted a blowout quarter: Q4 revenue +39% YoY, driven by AI server demand.

Why it matters: Growth alone isn’t enough anymore. Balance sheets and clean execution now matter in AI land.

₿ Bitcoin stalls below $70K

Bitcoin sits in the mid-$67Ks after a 6% surge earlier this week, fueled by a $323M short squeeze and $258M in ETF inflows.

Technically, BTC briefly reclaimed $68K but struggled near $70K resistance.

Two-thirds of derivatives traders remain long.

Why it matters: Risk appetite is alive — but positioning is crowded. Volatility risk is high if momentum fades.

🛢 Oil and gold climb on geopolitics + tariffs

Brent crude jumped to ~$72.25 (+~2%) as Middle East tensions and US–Iran developments added risk premium.

Gold pushed higher as well, supported by safe-haven flows and fresh tariff noise — including a new 10% global tariff with hints of possible increases.

Why it matters: Geopolitics and trade policy are back as structural market drivers — not background noise.

🏦 IMF backs the Fed’s slow-and-steady path

The IMF expects inflation to drift back toward 2% by early 2027 and supports gradual rate cuts to roughly 3.25–3.5% by end-2026.

Fed officials remain cautious, especially with tariffs potentially lifting goods prices again.

Why it matters: The bond market is balancing two forces — disinflation vs. policy risk.

💼 Labor market: cooling, not cracking

Initial jobless claims ticked up slightly to ~212K. Continuing claims actually fell.

Growth projections for 2026 still sit around 2.3%.

No panic signals — just moderation.

Why it matters: The soft-landing narrative remains intact. That gives the Fed flexibility.

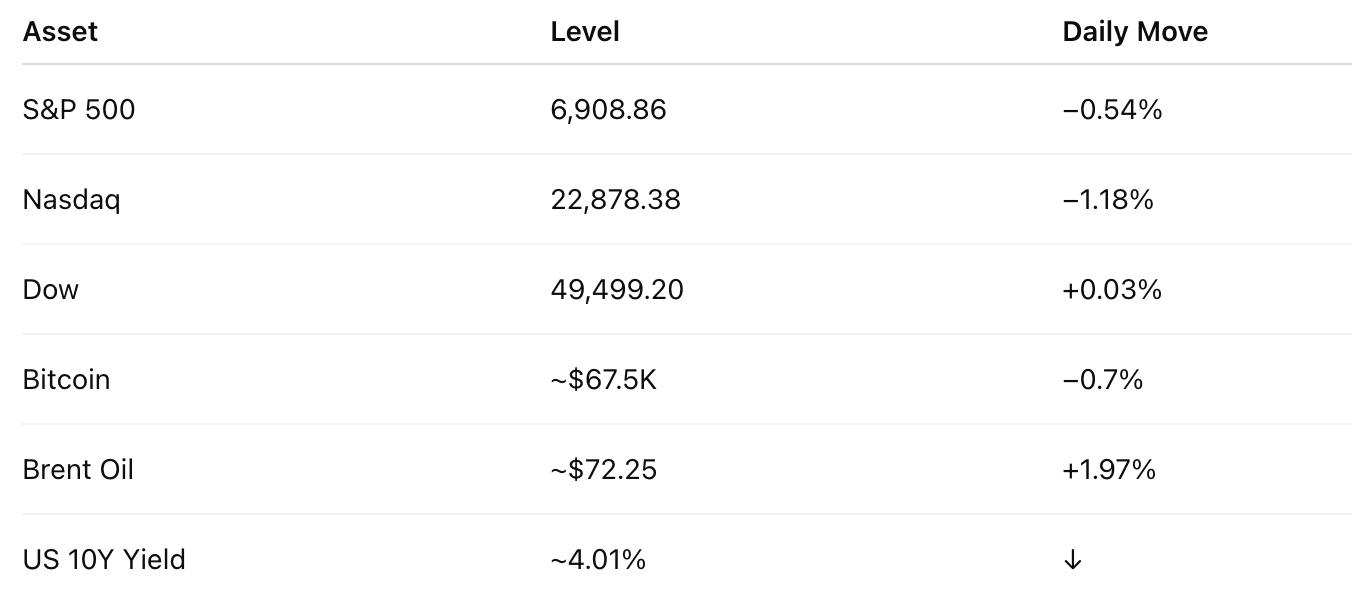

📊 Market Snapshot (26 Feb Close)

🧠 Big Picture

The market isn’t rolling over.

It’s maturing.

AI stocks are no longer one-way bets. Investors are demanding cleaner balance sheets, realistic guidance, and proof that earnings can justify valuations.

Meanwhile, bonds are sniffing out trade risk, commodities are reacting to geopolitics, and crypto is reminding everyone that liquidity still drives everything.

We’re not in risk-off mode.

We’re in price discovery mode.